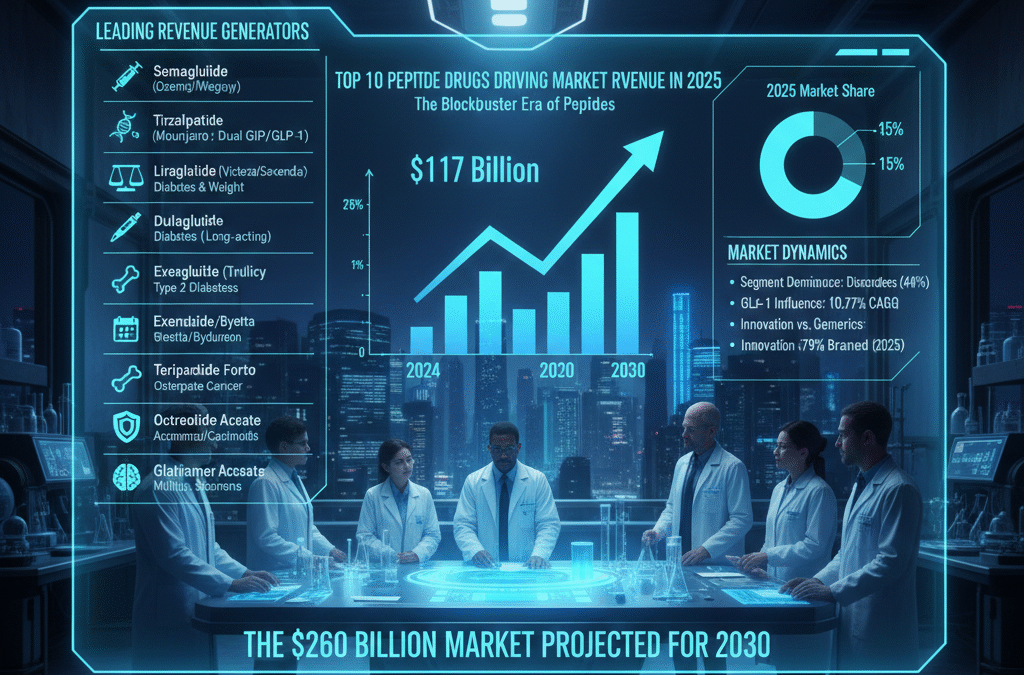

Introduction: The Blockbuster Era of Peptides

Peptide-based drugs have entered a true blockbuster era.

By 2025, several peptide therapeutics are generating multi-billion-dollar annual revenues, reshaping pharmaceutical market dynamics.

Rather than niche treatments, these drugs now anchor entire therapeutic categories. Together, they define commercial success across metabolic disease, oncology, endocrinology, and neurology.

Leading Revenue-Generating Peptide Drugs

Below are the top peptide drugs driving global market revenue in 2025, listed by impact and commercial significance.

1. Semaglutide (Ozempic / Wegovy)

- Manufacturer: Novo Nordisk

- Indications: Type 2 diabetes, obesity

Semaglutide remains the highest-revenue peptide drug globally.

Its dominance in both diabetes and obesity treatment is driving Novo Nordisk’s projected peptide revenue toward $55 billion by 2030.

2. Tirzepatide (Mounjaro)

- Manufacturer: Eli Lilly

- Indications: Diabetes, obesity (dual GIP/GLP-1 agonist)

Tirzepatide continues to disrupt the metabolic market.

As a dual-agonist peptide, it delivers superior outcomes and is a primary contributor to Eli Lilly’s projected $42 billion peptide revenue by 2030.

3. Liraglutide (Victoza / Saxenda)

- Manufacturer: Novo Nordisk

- Indications: Type 2 diabetes, weight management

Although facing generic competition due to patent expiration, Liraglutide remains a foundational revenue driver and helped pave the way for modern GLP-1 dominance.

4. Insulin Glargine (Lantus)

- Manufacturer: Sanofi

- Indications: Long-acting insulin for diabetes

Lantus remains one of the longest-standing peptide blockbusters.

Despite biosimilar pressure, it continues to generate substantial revenue within Sanofi’s $12 billion peptide franchise.

5. Dulaglutide (Trulicity)

- Manufacturer: Eli Lilly

- Indications: Type 2 diabetes

As a once-weekly GLP-1 agonist, Trulicity maintains a strong position in the metabolic market and remains a key contributor to Eli Lilly’s peptide portfolio.

6. Exenatide (Byetta / Bydureon)

- Manufacturer: AstraZeneca

- Indications: Type 2 diabetes

Exenatide remains part of AstraZeneca’s $8 billion peptide portfolio, although patent expirations are gradually shifting its market share.

7. Teriparatide (Forteo)

- Indications: Osteoporosis

As a parathyroid hormone analogue, Teriparatide remains a major player in bone health. However, increasing biosimilar competition is reshaping pricing and access.

8. Leuprolide Acetate (Lupron)

- Indications: Prostate cancer, endometriosis

Lupron continues to be a major revenue contributor within the oncology peptide segment, which is projected to reach $52 billion by 2030.

9. Octreotide (Sandostatin)

- Indications: Acromegaly, carcinoid tumors

Octreotide remains a cornerstone therapy in specialty endocrinology and oncology, maintaining relevance despite newer therapeutic entrants.

10. Glatiramer Acetate (Copaxone)

- Indications: Multiple sclerosis

Copaxone highlights the importance of peptides in neurological and immune-mediated disease management, maintaining steady demand in a competitive market.

Market Dynamics Behind the Top Peptide Drugs

Several macro-trends explain why these drugs dominate revenue charts.

Metabolic Disorder Dominance

Metabolic disease treatments account for approximately 44% of total peptide market revenue, representing $52 billion in 2024 alone.

The GLP-1 Effect

The global GLP-1 revolution is the primary engine behind the market’s 10.77% CAGR.

Obesity and diabetes therapies now represent the most lucrative segment in pharmaceutical history.

Innovation vs. Generics

Innovative branded peptides still hold 79.13% of market share ($92.7 billion).

However, biosimilar entry for drugs like Liraglutide and Exenatide is expanding patient access while forcing manufacturers to innovate next-generation therapies.

Conclusion

The top 10 peptide drugs represent the commercial backbone of the peptide therapeutics industry.

They address some of the world’s most prevalent chronic diseases while generating unprecedented pharmaceutical revenue.

As companies like Novo Nordisk and Eli Lilly continue expanding their pipelines, these blockbuster peptides will remain central pillars of the $260 billion peptide market projected for 2030.